At Context Analytics, we’re the leader in transforming unstructured, alternative financial data into actionable market signals. Our products are designed to surface insights that move markets—often in real time. One of the most powerful examples of this is the sentiment extracted from X (formerly Twitter), where conversations among investors, journalists, and the public provide a continuous stream of opinion around securities.

Our S-Factor Data captures this daily sentiment to help clients monitor breaking news, assess short-term risk, and identify trading opportunities. However, while S-Factor Data is typically delivered in daily buckets, we continuously explore how aggregating and transforming these metrics can produce a strong signal for longer-term holding periods- in this case, monthly.

Constructing the Long-Term Sentiment Momentum

We began by studying Raw Sentiment (Raw-S), one of the core metrics in our S-Factor dataset. Raw-S measures the raw sentiment score of conversation around a security over the previous 24 hours—positive vs. negative tone—without normalization for historical baseline.

To evaluate longer-term sentiment dynamics, we computed a monthly aggregate of Raw-S for each security in the price > $5 universe. Then, we applied a rolling window approach to capture multi-month trends.

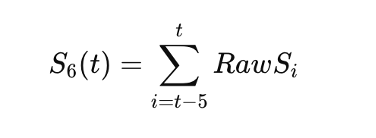

The six-month rolling sentiment sum for month t is defined as:

To measure momentum, we compared sentiment from the most recent six months with sentiment from the preceding six months:

This represents how much sentiment has increase or decreased over the past half year.

Interpreting the Signal

In essence, this metric quantifies the change in aggregate investor conviction over time—capturing a type of “first derivative” of sentiment that tracks velocity, not just direction.

Backtest Design

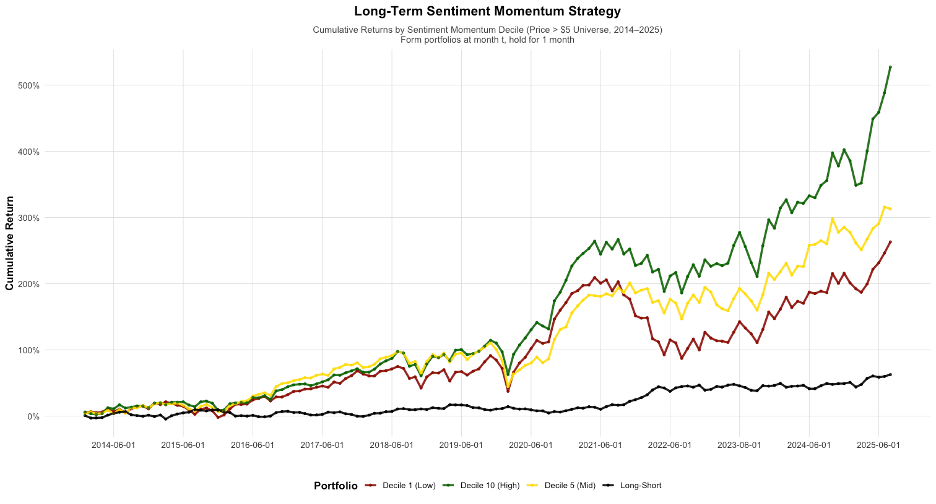

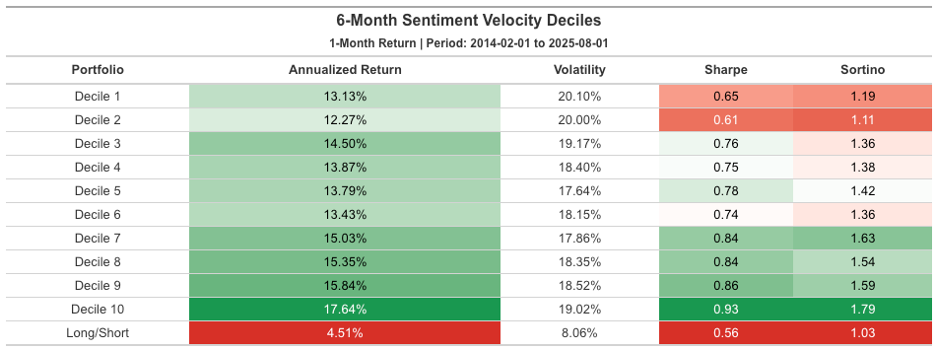

Each month, securities were sorted into deciles (D1–D10) based on their Sentiment Momentum value.

We then:

Results: Persistent Return Spread

The backtest revealed a near monotonic relationship between sentiment momentum and subsequent returns.

This suggests that sustained improvement in investor tone—as captured by long-term sentiment momentum—can serve as a predictive signal for future performance, even when using monthly holding periods.

Why It Works

From a behavioral finance perspective, sentiment inertia often extends beyond short-term reaction. Positive narratives build over time as news coverage, analyst commentary, and investor enthusiasm reinforce each other. This creates a feedback loop where improved sentiment continues to attract capital, driving momentum in both perception and price.

Conversely, fading sentiment can signal that a narrative is losing traction, even before fundamentals change—offering an early warning for declining performance.

Conclusion

Our research provides evidence that long-term sentiment momentum, derived from Context Analytics’ S-Factor Raw Sentiment, offers robust alpha potential for monthly investment horizons.

While our S-Factor data is most commonly used for short-term event-driven strategies, this study highlights how the same data can be feature-engineered into longer-term predictive signals.

Learn More

To learn more about how Context Analytics’ alternative data can enhance your investment strategies, visit https://www.contextanalytics-ai.com/ .