On April 14, 2026, Brazil's $EWZ ETF reached a new one-year high, driven by the critical resources uptrend and supply chain diversification. As major economies and companies seek to reduce dependence on Middle Eastern resources, Brazil's diversified and proven resource production capabilities position it for long-term success. The ETF has surged over 28% YTD, making it an attractive investment opportunity for those looking to tap into the global resources revolution. But for those tracking the Context Analytics Long Term S-Score, this milestone was not a surprise. The signal was there months before the headlines.

A Four-Phase Story, Told by the S-Score

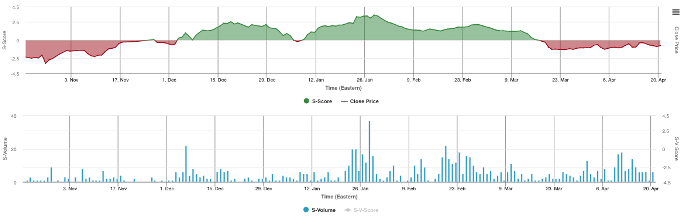

The Long-Term S-Score, one of Context Analytics' proprietary market sentiment indicators, tracked the EWZ narrative across four distinct phases over the past six months, demonstrating its value as a forward-looking signal rather than a lagging confirmation tool.

Phase 1 (October through mid-November 2025) was characterized by persistently negative sentiment, with the S-Score operating below zero throughout the period. Investors were cautious on Brazilian equities, and the data reflected it clearly.

The inflection came at the start of December 2025 (Phase 2). The S-Score crossed into positive territory and held there through the remainder of the year, well ahead of the explosive capital inflows that would define January and February 2026. This is precisely the type of early signal that separates sentiment analytics from backward-looking price data.

Phase 3 ran through January and most of February 2026. The S-Score moved consistently between 1.0 and 3.5, peaking near 3.4 in the final days of January. That strength was entirely consistent with the macro backdrop: the EWZ posted a 17% gain in January alone, its best monthly performance since 2020, while foreign capital inflows into Brazil's B3 exchange exceeded R$ 53 billion in Q1. Average daily trading volume on the B3 hit R$ 37.3 billion in February, up 50% year-over-year. Net inflows into the EWZ over the trailing three months reached US$ 1.63 billion, with six-month cumulative flows of US$ 2.22 billion. The Ibovespa touched all-time highs above 190,000 points in the final week of February, while the EWZ traded near US$ 40.

Phase 4 began with the escalation of the Middle East conflict in early March. The S-Score started deteriorating almost immediately, declining from 1.8 on March 1 to 1.4 by March 11, then moving into negative territory around March 17, closing the month at approximately -1.0. The shift in market tone was visible and measurable.

Why March Was Not a Straight Line Down

March was not homogeneous, and the S-Score reflected that nuance. In the first week of the conflict, Brazilian equities held up better than most emerging market peers, and the S-Score, while declining, did not collapse outright. The reason is structural: Brazil sits in an ambiguous position within a commodity shock. Petrobras carries significant weight in the EWZ, and the surge in crude oil prices (WTI jumped 33% in a single week, reaching US$ 94.65 per barrel by March 9) was a genuine tailwind for the energy-heavy index. Brazil is also a major exporter of agricultural commodities.

However, as the month progressed, the market began pricing in secondary risks. Brazil imports nearly all its fertilizer, with roughly half of supply transiting the Strait of Hormuz, representing a meaningful risk to its agribusiness sector. As those concerns compounded, the S-Score moved progressively lower, ending March in negative territory.

The comparison with other ETFs sharpens the picture. While the EWZ declined just 0.9% in March, the iShares MSCI Emerging Markets ETF (EEM) fell 9.2% over the same period. The South Korean equivalent EWY dropped nearly 19%, weighed down by its near-50% concentration in technology and semiconductor names. Brazil's heavier allocation to energy and materials acted as a natural buffer.

The Recovery: Flows Confirm the Sentiment Turn

With the gradual easing of geopolitical tensions and growing expectations for a US-Iran ceasefire, global markets staged a strong recovery in the second week of April. In the week ending April 10, investors allocated over US$ 1.1 billion into US-listed emerging market ETFs, breaking a four-week outflow streak that had totaled more than US$ 5.6 billion. The MSCI Emerging Markets Index rose 7.4% that week, its strongest weekly performance since June 2020.

Brazil led all emerging markets in flows. The EWZ received US$ 632.9 million in net inflows for the week. On Friday April 10 alone, the fund attracted US$ 241 million, the largest single-day inflow since 2019. On Monday April 14, that record was broken again with US$ 337 million in a single session, the highest daily inflow since May 2017.

The Ibovespa has now set 17 consecutive all-time highs in 2026, briefly touching 199,000 points intraday, with the Brazilian real strengthening below R$ 5.00 per dollar for the first time in two years. Year-to-date foreign flows into Brazilian equities have exceeded R$ 60 billion as of early April.

According to data compiled by Bridgewise, the EWZ's YTD return of over 28% ranks as the second-best performance across a broad sample of developed and emerging market ETFs tracked globally, trailing only the EWY, which has surged approximately 45% YTD in a sharp technical recovery following its steep March selloff.

The Takeaway for Sentiment-Driven Investors

The EWZ narrative over the past six months is a textbook case for why sentiment analytics deserves a seat alongside traditional fundamental and technical analysis. The S-Score's positive inflection in early December 2025 preceded the surge by weeks. Its gradual deterioration through March signaled a shift in market tone before flows reversed. And the broader macro thesis, a commodity-rich economy with falling interest rates, insulated Brazil's equity market from the worst of the geopolitical shock.

For investors and analysts looking to get ahead of macro-driven ETF moves, especially in resource-intensive emerging markets, the S-Score continues to demonstrate its value as a leading indicator. Brazil's positioning as a beneficiary of both the global resources revolution and the regional rate-cutting cycle makes it a compelling test case for sentiment-driven frameworks going forward.