Social Market Analytics recently released a SPAC sentiment dataset. This dataset is comprised of all SPACs launched since September of 2017. We calculate our full social media metrics on these securities.

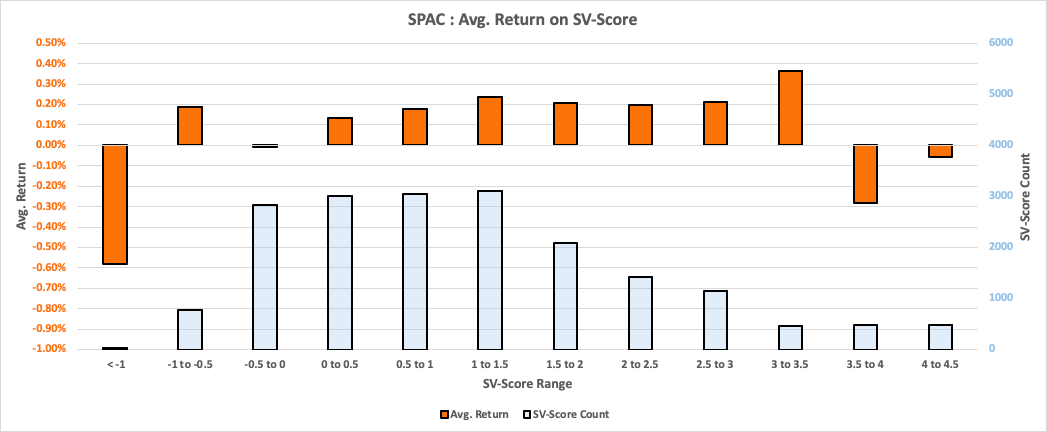

In the chart below we looked at subsequent 1-day returns (Close-to-Close) of all SPACs based on their SV-Score, which is a measurement of abnormal tweet volume for each security. The higher the SV-Score the more Tweets there are on that topic compared to its normal state. Scores were taken at 3:40 PM ET (20 mins before market close).

We found SPACs are especially sensitive to mentions on Twitter. The chart below is an overlay of subsequent close to close returns (orange bars & scale) bucketed by pre-close SV-Score buckets (blue bars & scale). We slice SV-Score in ranges of 0.5; most scores are between -0.5 to 1.5. The height of the light blue bar in the SV-Score Ranges represent the cumulative number of events in that bucket.

As a SPAC’s Twitter volume increases subsequent return increases as well. However, there is a point when new information is exhausted. When SV-Score rises above 3.5 standard deviations from its baseline mean, returns tend to underperform. If a SPAC is not generating social media buzz (SV-Score =< 0), it tends to underperform the rest of the SPAC market.

Monitoring SPACs on social media using SMA’s volume-based metrics can provide valuable insight into subsequent returns of SPAC securities.

For more information or to trial our data ContactUs@SocialMarketAnalytics.com